What is the carbon footprint disclosure obligation under CSRD all about? Who is affected, and how can you proceed? – EnExpert explains

Who is affected by the CSRD?

The Corporate Sustainability Reporting Directive (CSRD), a European Union directive on sustainability reporting by companies, has been in force since 5 January 2023. For some companies, this obligation is nothing new, as they have already been obliged to report on sustainability under the Non-Financial Reporting Directive (NFRD) since 2018. These companies must disclose their sustainability report on 1 January 2025 for the 2024 financial year. The CSRD also gradually obliges the following companies:

01.01.2026 → All other large companies must disclose the report for the 2025 financial year. These are companies with more than 250 employees on an annual average and/or more than €50 million in annual turnover and/or a balance sheet total of more than €25 million.

01.01.2027 → Listed small and medium-sized enterprises (SMEs) must disclose their report for the 2026 financial year (there is an “opt-out” option here).

01.01.2029 → The CSRD now also partially obliges non-EU companies, so-called third-country companies, to disclose their reports for the 2028 financial year. The obligation exists if these companies generate a net turnover in the EU of more than €150 million and have a branch or subsidiary within the EU. There is also a reporting obligation if the non-EU company or its EU subsidiaries are listed on a stock exchange in the EU.

Carbon Footprint Disclosure Obligation under CSRD

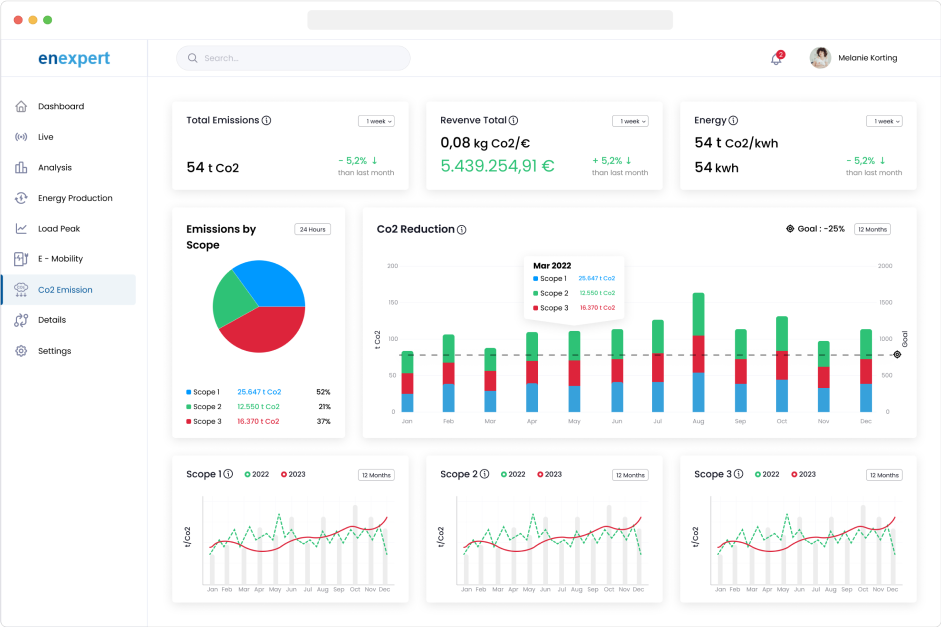

An essential part of sustainability reporting in accordance with CSRD is the disclosure of the carbon footprint. There are various standards, but within Europe and internationally the Greenhouse Gas (GHG) Protocols standard is the most commonly used. According to the GHG Protocol, emissions are divided into three areas. Let’s take a closer look at these scopes:

Scope 1 includes direct emissions, i.e. all emissions that originate from a source that is directly under the control or ownership of the company. Imagine, for example, that company vehicles emit emissions or that the company’s production facilities emit emissions.

Scope 2 therefore refers to indirect emissions from the purchase of energy such as electricity, steam, heating and cooling. This means that these emissions do not originate directly from the company’s operations or activities, but that the purchase and consumption of energy lead to these emissions.

Scope 3 refers to all other indirect emissions along the value chain. These include, in particular, emissions in connection with the purchase of goods and services, but also emissions from business travel, for example.

As you can see, the disclosure of the carbon footprint according to CSRD is relatively complex. However, please note the necessity of such measures to combat climate change. Only if companies have a detailed overview of their carbon footprint can they reduce it effectively and sustainably. There are various tools available to provide such an overview. The EnExpert Carbon Management System offers an efficient and GHG-compliant solution for the largely automated recording and balancing of your emissions.